Balancing act

Let's zoom out and see how it looks like from above.

This week came and went on really thing trading in the physical world as the industry gathered in London for IE Week, a venue for traders where you go to talk your book, get harassed by oil media vendors and get drunk on watered down cocktails. The lack of action was evident on the North Sea window with just a few offers and one deal, chartering activity in the Atlantic evaporated and futures and swaps volumes were slow to roll, and all of this while flat prices were slamming back and forth as the news came by.

February seaborne crude oil import ended in a much positive note, with a caveat, this sudden increase for China is no more than backlogged Russian and Iranian January barrels that eventually found a safe port, some of them going further south of Shandong, some VLCCs STSs, a new port operator in Yantai, the usual stuff. Bear in mind that yesterday Feb 27, the grace period for discharging OFAC sanctioned tankers expired, so now we are going to see what’s what.

OFAC came back with more sanctions on Iran, 13 vessels and a bunch of middle men, so did the EU and UK on Russian assets, and the market quickly shrug it off.. I guess the word “Sanctions” doesn’t carry the same weight as is used to a few weeks ago.

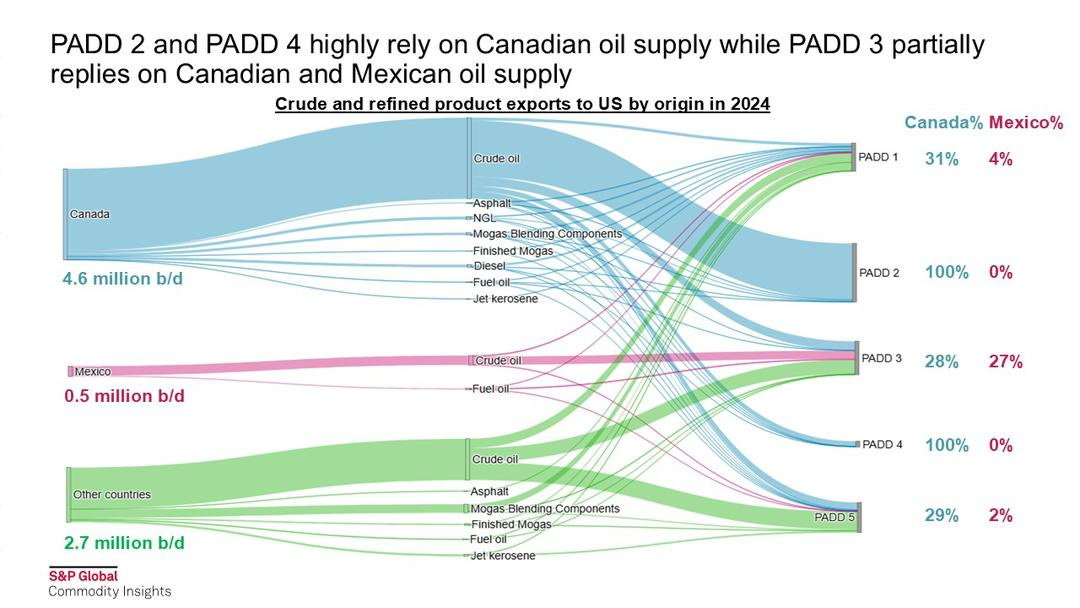

The word tariffs is what is making the oil (and the broader) markets more itchy, we had a big one this week but no one could say they didn’t see this one coming, revoking Venezuela’s export licenses (better known as the Chevron waiver) will definitively have some impact, as one of the main imports of the precious heavier sour crude into the US Gulf coast is coming from there. It will further tighten the balance of the heavier molecules even further.

Is not impossible to replace as we are talking 200/300kbd, which will be shifted (not all of them) to Asia on the parallel market, but is not impossible to replace those barrels for the US, they just need to pick up neighboring Canadian and Mexi…. no, wait a minute... Trump just hinted tariffs are kicking in next week for Canada and Mexico.

The headline caused gasoline and diesel cracks to jump, on the notion of US refineries running a lighter slate, leading to reduced distillates availability. 30% of the market thinks Trump will go through with the tariffs, 30% thinks they will be postponed once again, and the remaining third is drunk at the IE week.

The other major thing on the horizon is the OPEC decision to unwind the cuts in Q2, which I was convinced they will actually start pumping more, but as focus shifts back to demand once again, I’m leaning towards the idea that they will delay the return of these barrels, but they won’t... I mean, they will announce it citing market conditions etc.. but in reality they will be start pumping more, actually, they already are. UAEs is back at it again producing almost 1Mnbd above the quota and ADNOC announcing they are ready to pump more murban barrels, Kazakhstan openly said is adding 250kbd from Chevron’s field expansion, Nigeria is bragging they are now producing 1.8Mnbpd, and though not capped by quotas, these are 300kbd the Cartel wasn’t accounting for.

And why shouldn’t they? Last weeks we saw a lot of announcements from big oil companies (BP, CVX, Galp, XOM, PBR) expanding exploration, production and field maintenance, buying FPSOs. This low volatility, 70s range oil works for producers, they do make money at 70, is not as much as last two years but is something, there aren’t that many Free Cash Flow generating investments, and the green agenda is definitively out. So, my word to OPEC people, they better get on with the times, because the real threat is not coming from the West.

Anyhow, let’s leave aside the news flow and focus on pure market dynamics, which is in a state of flux. Right around this time of the year, the tectonic plates are shifting beneath the feet of the oil markets. I put it graphically so we can understand what has been going on and what I expect for the next month.

It’s all about refinery turn arounds and how the different regions offset each other, we can see that clearly with the oil balances. The US is wrapping up the maintenance season in PADD3, while Asia is also starting to ramp up, a little bit behind, and now is Europe who is entering this phase.

For what concerns the crude oil markets, we are out of the woods. Refining turnarounds are over, since the oil buying is now past April/ mid-May. The weakness we saw in the last 6 weeks in trading, premiums, diffs.. etc, was because those barrels were landing in Europe now. Strength in Dubai was the first one to kick into gear because Asia was buying March deliveries, past the turnarounds, and the US is still battling in PADD1/2 but PADD3 is almost done.

Assuming demand is flat, which it was except for weather events, product inventories behaved the same way, see the interplay between products and regions, Americas builds, Asia draws, Europe builds light ends, Asia draws and so one.

Two of the major producing and consuming regions are into crude buying mode, and the best part is, the refining margins are actually pretty good all things considered, even Chinese teapots are making money, so when they are back, they will be back with vengeance, trying to capture these profits, which, as you know, it will start killing the spreads, which will lead to more cautious crude buying, and we start all over again. These cycles take 8 to 10 weeks to play out, enough time to underpin current oil markets that seem a little loose at the moment. Within paper markets there is already evidence of tightening and some prices will have to move around.

Of Course, this all could change in a wimp with a reawakening of the tariff wars, China though doing better is still in a delicate position, The mood about settling the Ukrainian conflict changes every day, the path towards normalization is still a long one.

Elsewhere, oil finishes the second month of the year with a two dollar drop, not bad at all if you remember what people were saying back then about building 1.5Mnbpd in Q1.