Compounding Errors

A tale of a shortsighted market

Things are moving way too fast, but even in the fog of war we can already see a few things more clearly. Now we actually have certainty about the objective behind this whole feat and I’m not talking about Trump, I mean the Iranians. They set a clear goal for the barrel at $200… and that’s the direction of travel.

Let me illustrate how serious the situation is.

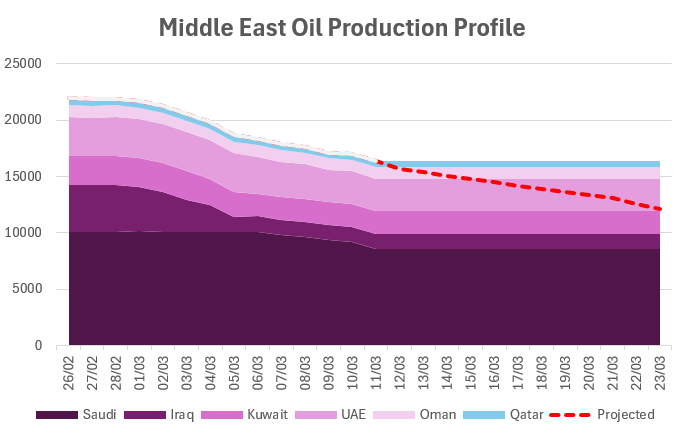

As of today more than 5Mnbpd of crude and condensate production has been lost. Every day that goes by is one less VLCC that can load, and with terminal tanks already close to full we will likely see more precautionary shut ins.

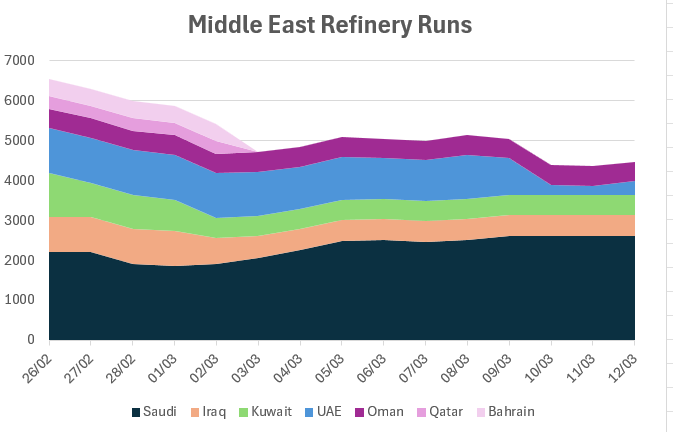

Maybe on the crude side we are not really feeling it yet, but in refined products, where around 1.9Mbpd has already been lost just in the Middle East. What we are seeing in Jet and gasoil is stressful, and Jet will likely be the first product to start testing the limits of demand destruction.

Let’s analyze this supply gap that has now been running for two weeks and to understand it properly we need to separate what is not being produced, around 5Mbpd, from what is not flowing through the Strait of Hormuz, roughly 13Mbpd.

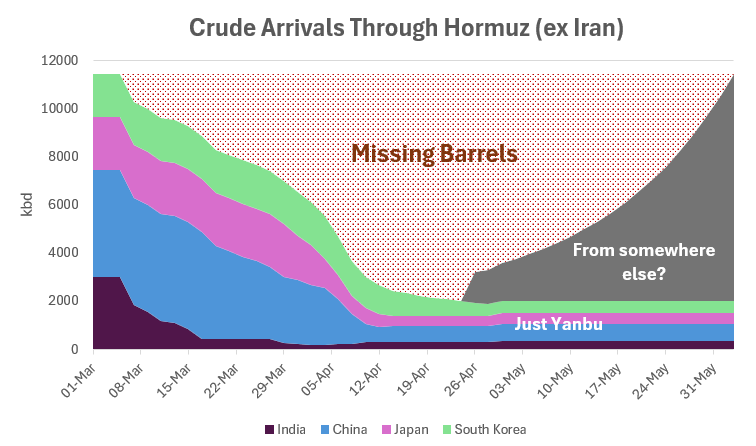

So why is the market so complacent? Because it sees around 120M barrels already loaded inside the Persian Gulf, ready to sail the moment the gate opens. The market assumes all that supply will hit at once and push down the flat Price, the differentials and freight, and everything will go back to normal as soon as Trump declares victory… well… not really.

This is a graphical representation of the problem. Since transit through Hormuz stopped, barrels that do not arrive from the Middle East are barrels that will not arrive from anywhere else, leaving a gap that has to be covered by the SPR. Alternative barrels from the Atlantic, even if they started loading today, will take time to land. Even the Yanbu bypass is not enough, assuming a realistic 3Mnbpd, and excluding the Murban and Oman baseload that already moves outside the Strait.

This time transit time actually plays in favor of Korea, Japan and China because they have more time to prepare. India, Pakistan and Bangladesh did not have time to react. I can understand Pakistan and Bangladesh, they are always close to the edge, but India? The second largest crude importer and with no strategic stocks to speak of. Today everyone is paying the price for that kind of miscalculation.

That gap is roughly 240 million barrels. Over 44 days that is almost 6Mbpd if this is not solved immediately. If the Strait reopened TOMORROW, that grey area on the right would simply move further to the right, shrinking the gap. The problem is that this is a commercial decision that needs to be made TODAY… and I’m not seeing it yet (more on that later). India does have the advantage of proximity and can decide later.

Anyway, Japan and Korea decided to roll the dice and release inventories, betting that transit will normalize in the next few days. That strategy could easily backfire.

China on the other hand has its own SPR of sanctioned barrels, roughly 70 million, but interestingly Unipec requested to use those reserves and the request was denied. China may be playing a different game here. It could be waiting for the US to release 172 million barrels into the Gulf, where barrels are currently abundant. That would likely crush WTI Houston relative to other benchmarks, creating a perfect opportunity to transfer barrels from the US SPR into China SPR. When the IEA eventually needs to refill those barrels, China will be sitting on a mountain of them… very clever.

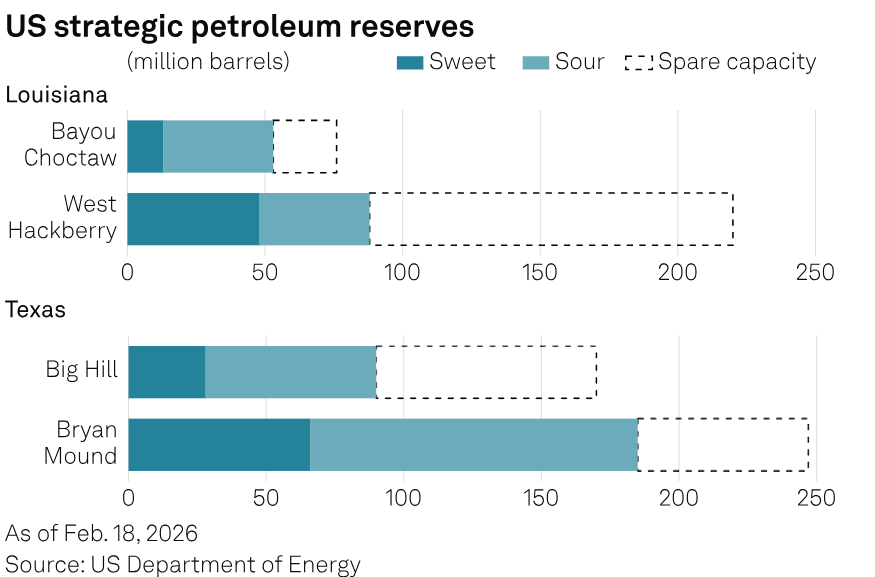

So does releasing 400 million barrels actually work? That is only around 1.5Mnbpd in a 10Mnbpd supply void. It could absorb some of the shock only if transit resumes immediately, otherwise it is basically irrelevant. The market has already delivered its verdict. The good news is that what sits in US tanks is mostly sour, which is exactly what the market is missing, but its effect will mostly show up in differentials depending on the release pace. The main issue is still time and location. The barrels are needed in Asia Pacific, and they are needed right now.

Europe holds more products in reserve than crude, which could relieve some pressure in gasoil, but jet remains a problem. Jet logistics are complicated, storage options are limited, and there are very few specialized tanks available.

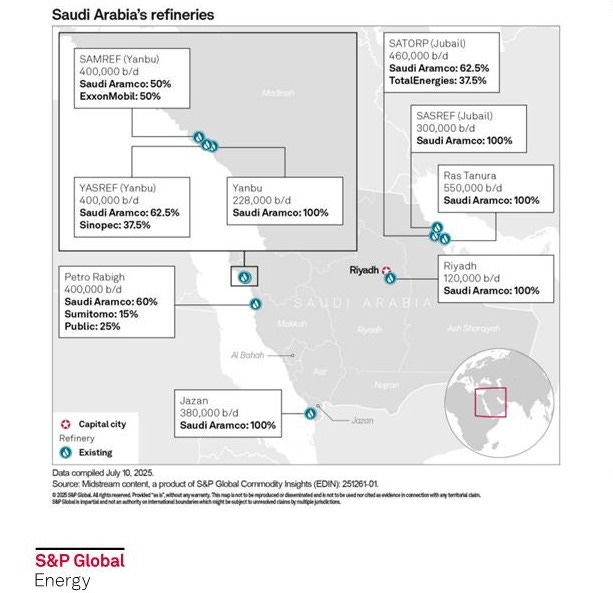

This week we all learned a new word… “Yanbu”. But what the hell is that?

Yanbu is currently Saudi Arabia’s only export outlet. It is where the East-West pipeline ends, with a theoretical capacity of 7Mnbpd. That said, this line has never really run at full capacity, and that does not mean all of it is export capacity. The pipeline was built for rainy days like today, but also to feed the refinery complex along the Red Sea coast. Not exclusively, because there used to be a lot of intercountry traffic with smaller ships loading in Ras Tanura. That traffic has also stopped, so Saudi Arabia now has to choose between exporting crude or supplying its refineries.

For now it seems they are prioritizing Asian customers, and we are not seeing more than about 2.5Mnbpd. There are two terminals with a combined capacity of 4.5Mnbpd. The historical maximum was around 4Mnbpd and that was with smaller ships. Berthing a VLCC takes much longer than a Handy, which matters when you measure things in barrels per day. For now though it is the only viable option, and even more reliable than Fujairah and Duqm in Oman, which have been loading intermittently. The fact that this pipeline spits mostly Arab Light is less than an issue when the market is starving, but could create a bottleneck in Arab Heavy and mediums if those barrels can’t get out.

Repealing Jones Act? I won’t even entertain that

Lifting Russian Sanctions? Nazdarovya!!

Putting all this into prices, with the oil glut now a thing of the past, in a balanced market Brent would probably trade somewhere between 75 and 85. In a market missing 2Mbpd, roughly what India is missing today, 90 to 100 makes sense. But a market short 5Mnbpd could be anything… 150… 200… who knows.

Can we actually get there? The truth is Iran does not need to do much more than it is already doing. At this point it depends on Trump, and I do not have high expectations. That said, we probably know the temperature where the TACO gets fried… somewhere around 130 to 150.

We are barely at $100 and people are already talking about demand destruction in emerging markets. There is even talk of rationing across OECD countries. That says more about the fragility of the global economy than anything else. These prices are not far from the average of 2023. That is why I doubt we see anything much beyond $150 for a sustained period. At those levels you will easily get 5 to 6Mnbpd of demand destruction.

Jet will do its part in the western hemisphere, while road fuels and LPG will do theirs in Asia Pacific. It has not even been two weeks and there are already people who cannot afford to heat their food. Imagine if this drags on for a few more weeks. The damage already done to the global economy is irreversible.

Keep reading with a 7-day free trial

Subscribe to Oil not dead to keep reading this post and get 7 days of free access to the full post archives.