Last week we ended on a more constructive note, albeit highlighting the positive correlation between flat prices and equities markets that was dragging sentiment down, but this week we finally broke free, as oil markets divorced from the US indices since Monday.

The strength in the physical, or what we call the physical paper, Dated, time spreads, cracks eventually caught to flat price and oil is ending this short week with a substantial gain.

What sparked the risk on according to analyst was a renewed effort from Trump / Secretary of Energy Mr. Wright squeezing even more on Iran, with sanctions to more tankers, a Chinese Teapot with no asset and threatening rhetoric, while at the same time praising the ongoing “indirect” talks between Iranian and US officials regarding their nuclear program, the Art of the Deal phase II?

None of that, the market couldn’t care less and is kind of tired of Trump tantrums, what I think it moved the markets was the signaling from OPEC that this time compensation from naughty over-producers is real, namely there is a firm commitment on Iraq and Kazakhstan this time.

The OPEC has updated its compensation mechanism, requiring seven members (Saudi Arabia, Russia, Iraq, UAE, Kuwait, Kazakhstan & Oman) to implement additional cuts totaling 369 kbd in monthly steps through June 2026 to offset earlier over production largely to counterbalance a the announced 411 kbd output rise a couple of weeks ago.

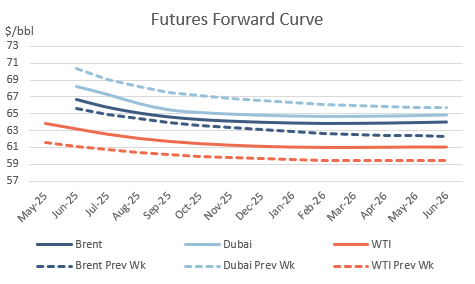

The illusion of OPEC back in command filtered the hesitating Dubai market, sending the cash premiums near $2 offsetting the debacle since the Saudis OSP smack down.

Nobody paid any attention either when OPEC cut its 2025 global oil demand growth forecast, now expecting a rise of just 1.30 million bd (down 150kbd from last month). The 2026 forecast was also trimmed to 1.28 million bd. Even less to the IEA that revised its 2025 global oil demand growth forecast downward to 730kbd, down 300kbd. Banks updated their price targets, downwards of course, and the market took it for what they are worth… muted reaction.

Not to say that global economy is not a concern going forward, but today the market is focused in the short term, and that is challenging some of those views, as we had some official info for countries like Türkiye, Brazil, India and some emerging markets that are showing resilience on road fuels... and that data is from when oil was at $75 and the DXY was at 110.

Peripheral economies learned to embrace volatility from the last Trump term in power, and they are riding this wave of neo-mercantilism rather well… if we learned something from COVID and the Russian sanctions is that the market adapts quicker and quicker every time, fears of a full-scale global recession are overblown. Surely some countries will get hit harder than others but on a global scale if oil is cheap enough, they will take it.

In oil you can sense some apprehensions of a slow down back in the curve, where the story is different than the one we see on the prompt, with time spreads flat, not only for oil but for every refined product as well, and in some cases falling in contango. It makes sense since “the prompt” is looking at the next two months at the most, any consequence of global trade halting will show up by mid-year at the earliest. For the moment refineries are making money, even the Chinese teapots are making money and that is a lot to say, so crude oil buying should continue.

When will I start to worry? When I start to see product inventories climbing week by week. So far, any weakness in core countries is counterbalanced by a pull from developing regions, case in point, the US as informed by the EIA this week is kind of lagging domestically with product supplied (as a measure of demand) is hitting historical lows for this time of the year, while at the same time gasoline and distillate inventories are being dried up by export outlets. Same with Europe and WAF, too much gasoline in ARA? No problem, Latam and Africa will take it.

As long as we keep this dynamic, crack spreads will hold, and as long as crack hold the physical market will still be itchy.

Although the short week in the West, there are some interesting stories going on that are shaping the prices we see on the screen, naphtha, fuel oil, tankers… Someone made money, someone lost a lot.

Keep reading with a 7-day free trial

Subscribe to Oil not dead to keep reading this post and get 7 days of free access to the full post archives.