The slow grind continues toward the previous trading range, with much of the anxiety now gone—except for a little back and forth on Canadian and Mexican tariffs, I think common sense will prevail. Feb 1st, Feb 18th? 25%, 10%? … who knows. Stupidity is unpredictable.

After a major blow to American exceptionalism over the weekend, things were put into perspective, including forward energy demand from AI data centers. This had been the major driver propelling natural gas prices and, in turn, supporting oil and oil products. Now, that effect is receding, also due to more favorable weather in the Northern Hemisphere. But that alone doesn’t explain this week’s softness in oil prices and spreads. It was an atypical week, with Eastern markets shutting down from Wednesday onward, only to return lightly on Friday, reconnecting with European and American benchmarks in a weaker tone. With a good chunk of the market absent, we cannot draw many conclusions, but interesting patterns have emerged as the first month of the year is already behind us.

Since we’re talking about China… something changed there.

We saw a change in strategy by mid-month from China. Although the seaborne import numbers look alarming, much of this could be attributed to Russian barrels still waiting to discharge. Some pushback from port operators, refineries, and middlemen handling these Russian cargoes persists. This resulted in an apparent trend snap, where, for the first time in months, they had to take oil from storage. Refining throughput remained steady at 14 Mbpd, imports at 9 Mbpd, and domestic production pegged at 4 Mbpd. That leaves us missing 1 Mbpd…

Some of these ESPO cargoes were diverted to southern ports in China rather than discharging in Shandong, moving to more compliant tank farms where they will ultimately be picked up by a sanctioned-free vessel back to Yantian Port. It’s not the most efficient supply chain, but as freight costs rise, something has to give.

We are seeing more barrels piling up on Chinese shores, but the biggest factor is Iranian barrels, which are facing difficulties clearing. Part of the issue is fear of sanctions blowback, but more likely, it comes down to pricing.

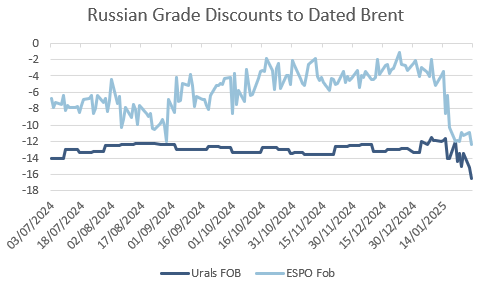

For Russia to keep pushing barrels to the water, some costs had to be absorbed. Paying $6 million for an Aframax from Kozmino on a four-day journey is not acceptable unless FOB prices drop—and they did. One of the easiest ways out for Putin was to bite the bullet and start selling crude under the price cap, which they did, with Urals reportedly selling just below $60, and ESPO bearing the brunt of higher tanker rates.

Things are still taking shape, and if you thought Russia would remain idle, you haven’t learned anything from the past three years. Old, rusty Aframaxes have been sold in the second-hand market (six since sanctions). I haven’t seen any STS yet, but there has been some repositioning of the unsanctioned dark fleet to the Far East. Russia is also shifting strategy toward exporting more refined products (e.g., gasoil and naphtha) even before new sanctions take effect, aiming to regain a foothold in the distillates trade. While Russian clean products are also subject to a price cap, they were never trading above it, even in a strong gasoil market. Their clean tanker dark fleet hasn’t been affected much, so this strategy makes sense—right? Well, it did until drone attacks resumed with renewed intensity over the past few days.

Refining runs rose by 2% (108,000 barrels per day) between January 15–19, reaching 754,800 metric tons per day—1.2% higher than the January 2024 average. The Kirishi refinery (owned by OFAC-sanctioned Surgutneftegaz) increased oil processing by 8% from December to January. Nevertheless, Russia’s offline primary oil refining capacity in January increased by 44% from December, meaning fewer refineries are operational, but those that remain are running harder.

Moving away from Russia’s struggles—concerns mostly relevant to India—we find ourselves with a tale of two markets. On one side, we have the lighter grades (WTI, Brent), which are starting to be offered more aggressively as we approach what looks like a heavy maintenance season in both the U.S. and Europe. This is especially true in the U.S. Gulf Coast (PADD III), where refiners were running at full tilt for most of the winter. Gasoline build-ups—ring a bell?

On the other hand, we have heavy/medium sour crudes holding a steady course. Dubai’s action didn’t take a break, and differentials for Middle Eastern, West African, or Latin American grades remain firm regardless of benchmark movements in flat prices. I estimate that some 300 kbd of Urals will be lost over the next two months, and it will take time for those barrels to return.

Next week will be a moment of truth for the Middle East, as we await Saudi Arabia’s March OSPs. Will they dare to price their crude according to the current spot market? If they use the M1/M3 spread and cash premiums, we should expect at least a $3.50 increase. Remember, February premiums were just $0.60. How will the Chinese react? They didn’t like the 60-cent price increase in February and cut allocations by 1 Mbpd. (Unipec and PetroChina selling partials in Dubai is a hint.)

We’re already seeing increased Chinese inquiries for crude from the Americas, West Africa, and even the long-forgotten CPC from Kazakhstan, which is trading at Dated -$4! This comes at a time when Kazakhstan has reached a record-high production of 2 Mbpd. Now, just imagine if the Red Sea opens up and Suezmaxes start flowing east again… something like that may be in the cards.

And then there’s the OPEC+ meeting. Will they continue to hold back? I’m not sure they’ll have another chance to sell oil at a $5 premium while also pleasing Trump and starting off on the right foot. Everything is pointing toward more barrels in Q2, and that’s weighing on traders’ minds.

As we speak, Big Oil is presenting Q4 2024 results—with mixed emotions. Big gains in oil production, but weak numbers in refining and trading. Expected, right?

The Year of the Wooden Snake begins with political strife, backroom deals, and uncertainty about the course of the global economy. One thing is sure, tariffs are coming!