Dire Straits

Oil physical in trouble

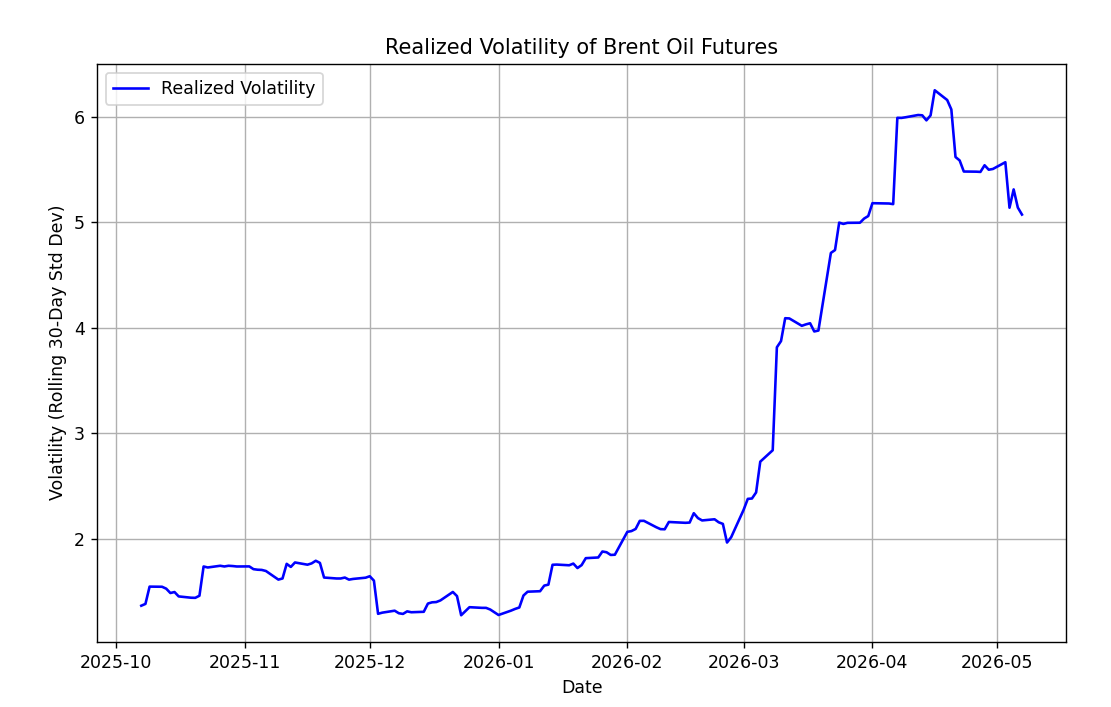

At this point I do not think is worth talking about ceasefires, attacks, negotiations and all that noise, the market is slowly shrugging off the headlines and as a consequence we are getting these violent swings that, rather than attracting traders, are sending them to trade INTC or whatever the kids trade these days... nothing new there, but now this apathy is spreading into the physical markets as well, where traded volumes have also been halved, although unlike futures and with far less volatility, dedicated swaps (CFDs, DFLs, crack spreads, E/Ws) are also lingering. We might have reached the saturation point where price itself no longer seems to matter.

Following up on last week’s discussion, where we argued that demand may be overstated, it is time to talk about supply and ask whether we are actually underestimating supply, because there has to be a reason why oil is trading at just $100, right?

Since this whole saga began we have always talked about fear, fear of running out of barrels, fear of shutting down a refinery, fear of crossing the strait, but this industry is not driven by fear, it is purely on greed.

Where did these barrels come from? The obvious answer is SPRs, but if we look at the actual numbers awarded, they do not even reach 100 million barrels hitting the spot markets. So then what, more production? No, you cannot suddenly produce 2Mnbpd overnight.

From inventories then? Yes, but question is from which inventories, because you have tanks.. and tanks. We tend to think of the oil market as a global system that always balances itself, which it is, but in reality it is a system made up of subsystems, and those are domestic markets.

Lately, what export programs have been showing, (whenever they are available), is one or two additional cargoes squeezing into the terminal schedules, that cannot be explained by higher production or visible inventories, which makes me think these are barrels diverted away from domestic refining system and pushed into the export market instead. Why would they do that? Because exports pay more, always does. Nigeria, Libya, Argentina, Brazil come to mind. These countries share the characteristic of having lower elasticity, where demand falls before refiners adjust output, and as a trader that gives you a window to capture better pricing. Export prices are generally higher than domestic ones because they trade on the spot market and can always ask for a FOB premium, unlike domestic sales that run on monthly averages… of course they have supply commitments but they can take advantage of small producers that don’t have terminal access or enough capacity to fill a crude oil tanker.. oil trading is all about fu**ing someone over.

And what about the poor people in those countries who will end up with fewer domestic products?…Tough luck.

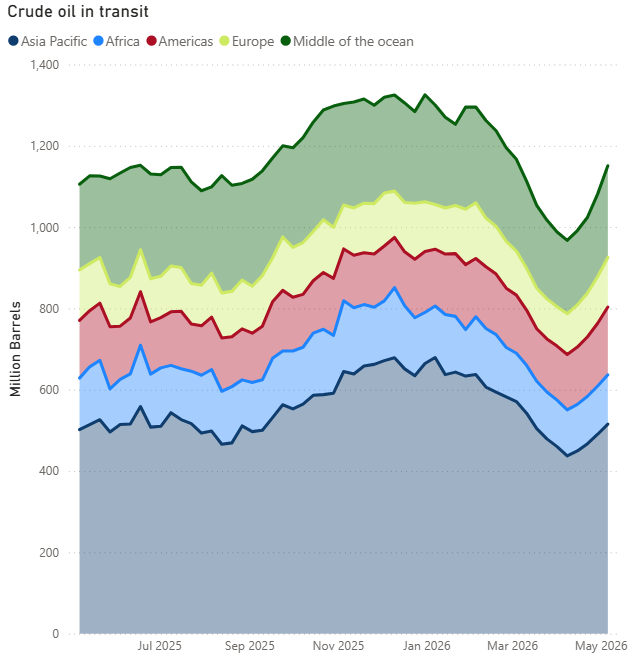

That explains why we saw some extra cargoes that were never planned, but the most important part is what we do not see, and things that were rumors a few weeks ago are now starting to get confirmed, there are vessels that exited the strait without us capturing them on shiptrackers. Of course all of this is very recent and still impossible to quantify, but there are more barrels out there than we are being told.

Shiptrackers. We got used to take shiptracking volumes as gospel, but if you know how they work, those are mostly estimates, quite accurate, but 50% is modelled by algos.. which take vessel fixtures, reported draft (how much a vessel is sunk in the water) and loading programs, some Agent reports and they come up with a volume calculation. In oil trading there is clause called MOLCO, more or less on charterers options, which gives the charterer (the exporter, if you will) the operational tolerance to load -5/+5% of the contracted volume. When you have a market like we have with at some point $15/bbl of backwardation, if you are loading a vessel you will try to fill it to the brim.. you can even bribe the captain and the surveyor and throw even a little more.. but please don’t do that (they’ve become very expensive). Point being, 20kb here 50kb there and that compounds… shiptrackers rely mostly on historical data to model “barrels on the water” so there’s that..

And that brings me back to China, where we theorized they might be using their SPR, maybe yes, maybe no, onshore tanks suggest they haven’t, but there is one piece I did not consider before and it may be the key to all this. We all roughly know they hold around 1.1 to 1.2 billion barrels of crude inventories, but what about refined products? There are no reliable estimates, not even speculation… but if refinery utilization drops by 3Mnbpd, products imports are negligible, and at the same time mobility data shows no meaningful change, except in jet, then those barrels have to be coming from somewhere. My suspicion now is that those stockpiles are China’s real buffer. Throughout 2025 and the first part of 2026, crude throughput remained well above implied demand, they probably built more than 500mb.

How much is left in the tank? Impossible to know, but the fact they granted additional export quotas may give us some clues, and the reality is that today they are not buying oil for July deliveries.

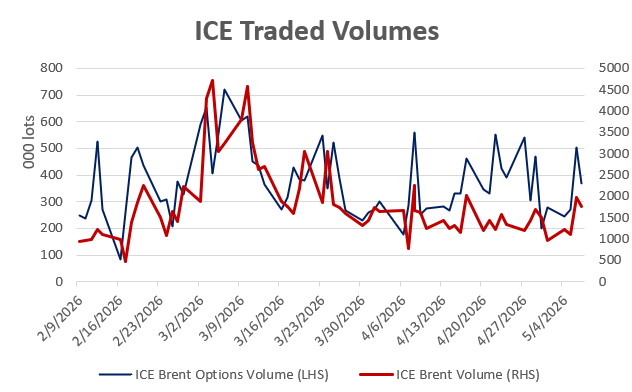

Now, why is nobody trading oil futures?

Recently traded volumes have dropped sharply, but the correlation between options and futures has started to tilt more toward options, suggesting that a large part of risk management may now be moving through that market.

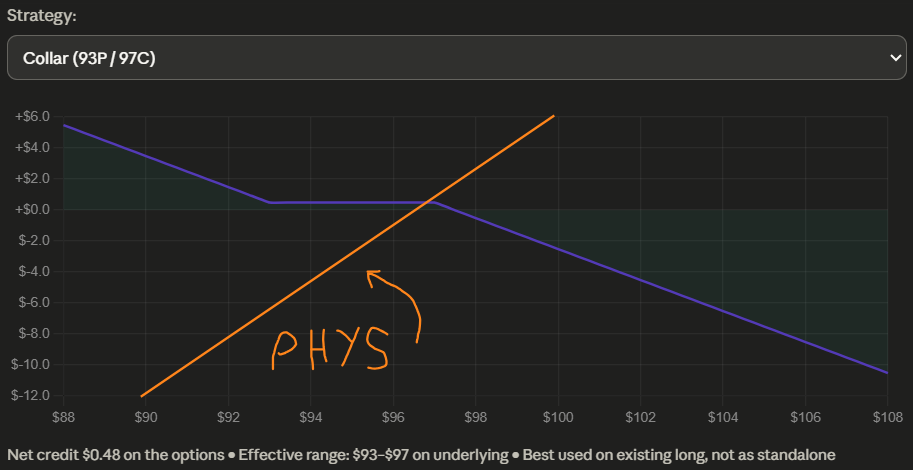

If we consider today’s market setup, where there is an underlying fear that the strait could reopen and prices could drop $10, while at the same time there remains a still possible, though increasingly smaller, chance that everything blows up again and we get another spike, then a strategy that limits downside while preserving upside, like a collar, becomes much more effective.

Take the case of an Asian refiner, if they buy a WTI cargo, meaning they are physically long, instead of selling futures against Dubai they could structure something through options and completely eliminate basis risk, which today, with broken benchmarks, is probably the biggest concern across the oil market.

The point is, we do not have full visibility into what is happening, and there are players with far more information than we have, so we have to assume the price is probably right.

Keep reading with a 7-day free trial

Subscribe to Oil not dead to keep reading this post and get 7 days of free access to the full post archives.