Drifting Away

Can we live without Hormuz?

This week gave us proof that this is still far from resolved, reflected in what was probably the strangest ceasefire in history... and every time an agreement appears imminent, Iran asks for just one more concession that pushes any potential understanding further away... and then there is Bibi.

Yet the market keeps weakening, and now it is no longer just the flat price, cash diffs for both crude and products are telling us that things are Ok. Which means it is time to ask the question: can we live without Hormuz?

The entire price structure suggests a quick resolution, but the sentiment coming out of the Middle East says exactly the opposite, so the solution must come from somewhere else.

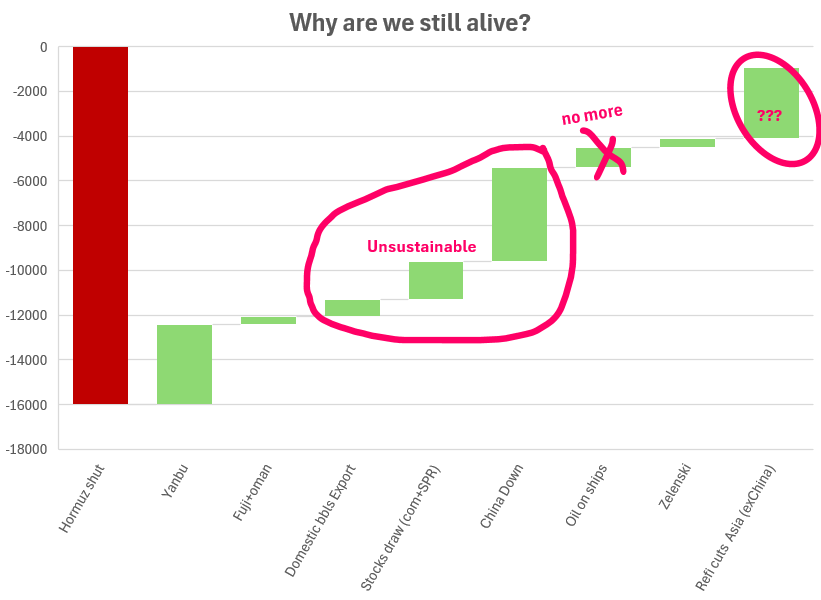

First, how did we get here?

The path that brought us to the current situation is clearly unsustainable, not in the medium term but right now. The exception could be China, which allegedly is not touching any of those SPR barrels and could probably survive for some time with lower imports, especially with refineries running at 70%. There are a few dark spots in the domestic demand numbers that support this theory: over the last month they cut the indicative price of gasoline and diesel three times... and demand is still not recovering despite refiners doing everything possible through aggressive destocking.

Beyond the strategic or planning angle, the reality is that all refineries are losing money. But why are they burning yuanes on every barrel they process? That led me to another theory... there is nothing strategic about this, it is purely economic and financial.

Bear with me, do we have less oil floating around? Yes, that is true. But there are still barrels available if you are willing to buy, even at a discount.

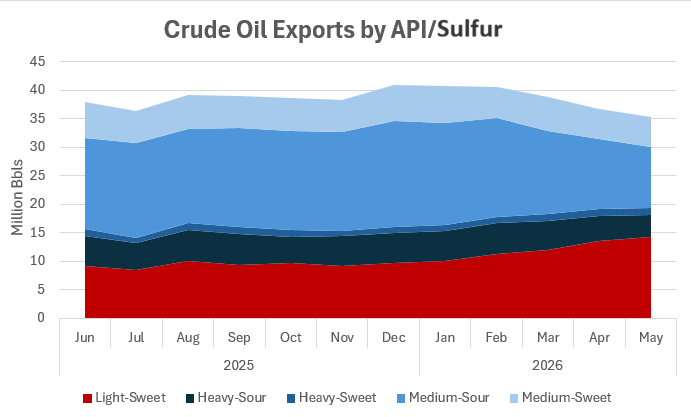

The problem is that all the additional barrels that entered the system over the last three months have been light sweets. China buys light sweets, it always has, but those barrels are not purchased to be run directly, they are used as blending feedstock for the heavier grades, which just happen to be the barrels missing from the market today. So if they have nothing to blend them with, why would they buy them?

Despite importing 4Mnbpd less than normal, China is taking everything with an API below 30, whether it comes from WAF, Canada, Iran, wherever. The overhangs are always light sweets. That does not mean they do not need them, it means they do not need them in that proportion.

Domestic production of 4.6Mnbpd carries an average API of 22° but relatively low sulfur content. What they buy from WAF is somewhat higher in API but similar in sulfur. However, the biggest shift in the quality slate came from the addition (forced?) of ESPO from Russia, a light sweet crude that pushed the average slate closer to 30° API, above the optimal range, displacing some purchases, particularly from WAF and the Meds.

Now, China managed to move a few ships out of the Persian Gulf over the last few weeks, medium and heavy sour grades, and then went out and bought some light sweet cargoes... coincidence?

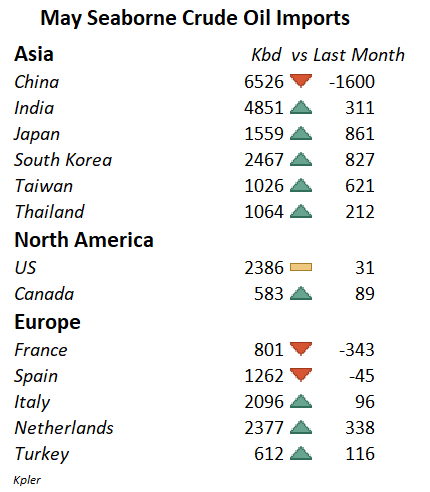

The other useful comparison is India, whose refinery configuration is remarkably similar to China’s. Has anyone heard anything about India over the last few months? They have their slate optimized with Urals, Venezuelan barrels, Arab Light from Yanbu, one or two weekly cargoes of some light sweet crude from WAF or Brazil and they are done.

The API issue can be partially solved, or at least postponed, with current crack spreads. The bigger problem, however, is sulfur content. The barrels currently trapped carry roughly 1.8% sulfur on average, the sour component. By running lower sulfur crudes, refiners are underutilizing a large portion of their conversion units, hydrocrackers, FCCs, delayed cokers, and so on. They are unable to convert residual streams into additional products, which ultimately impacts overall operating costs. That is where Chinese (and pretty much any Asian) refineries are losing money.

I would go as far as saying that what is missing today is not oil... it is sulfur.

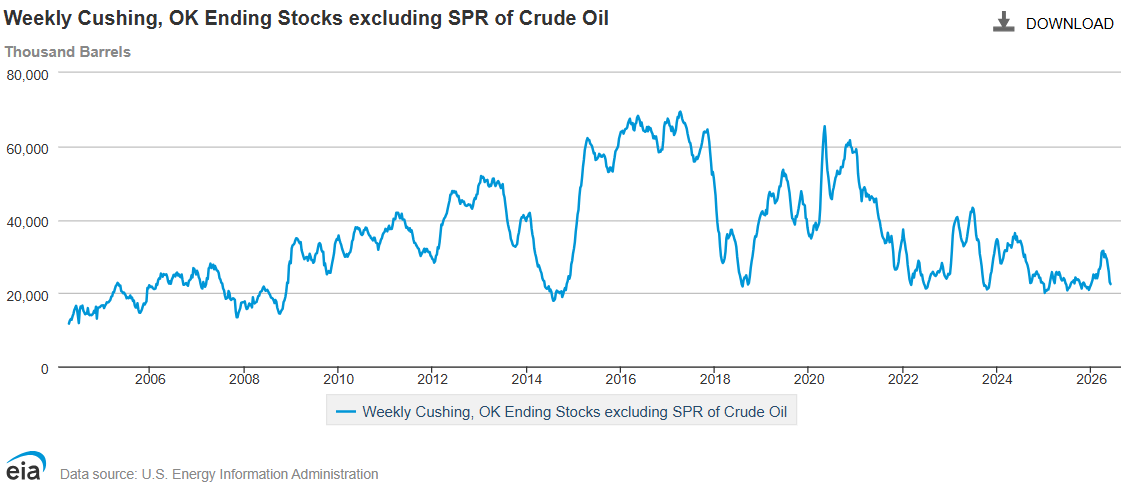

There are only two moments in an oil analyst’s life when it looks at Cushing inventories, the pricing point for WTI: when they hit 70mb or when they hit 20mb. The US domestic market is going to get spicy in the next few weeks... we are already seeing it in the Brent-WTI spread.

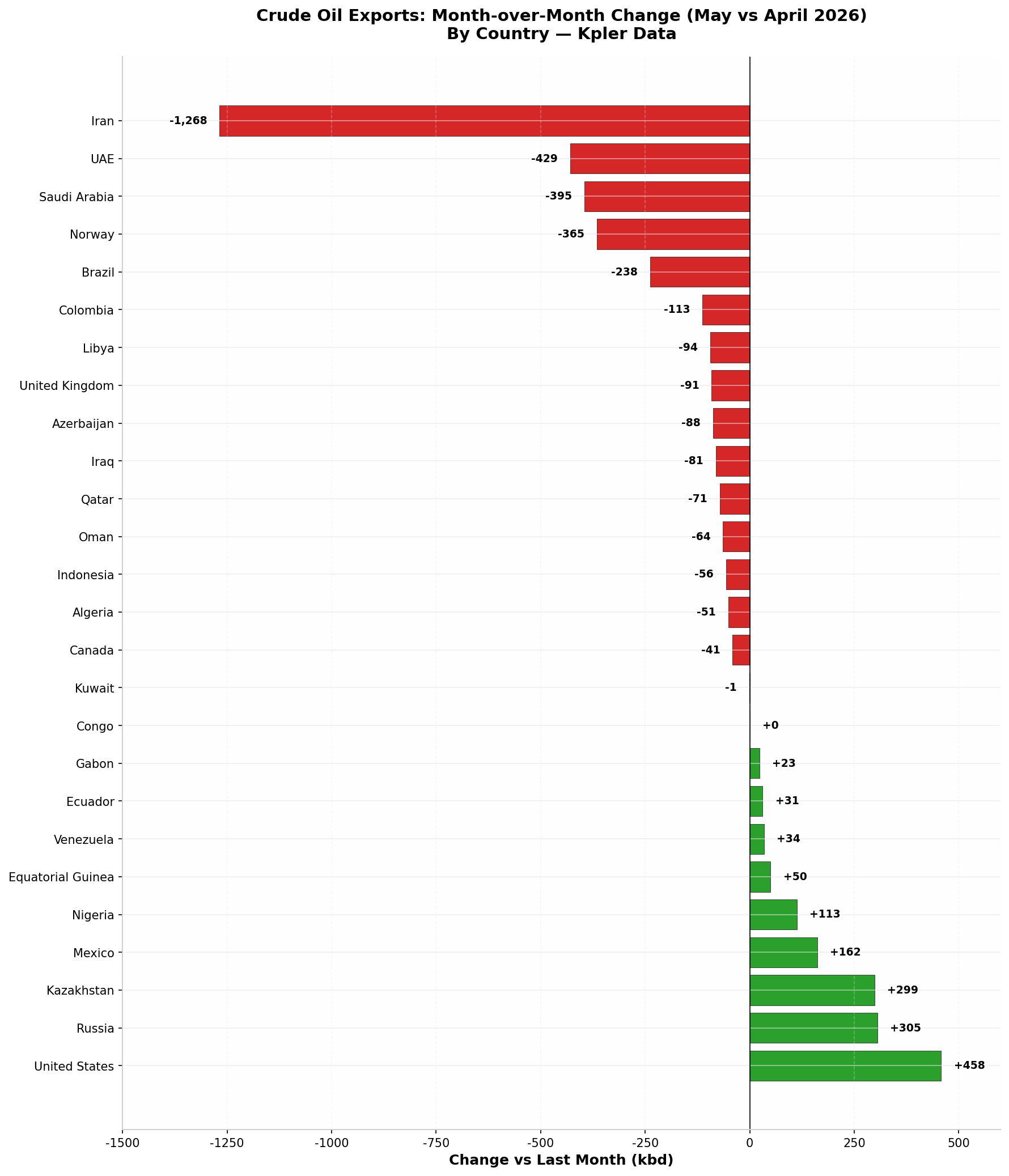

One thing that helped during April was that several exporting countries prioritized export markets over domestic demand, a dynamic also supported by lower refinery utilization rates in places like Brazil and Mexico. Well, that ended in May.

That small buffer is shrinking as more countries prefer to import fewer products amid growing concerns about the financial system and balance of payments pressures. DXY at 99, Treasuries at 5%…

We are already seeing some of this today... perhaps the wake up call will not come directly from the oil market, good luck with that SpaceX IPO.

And that brings me to the last point, should you want to warehouse risk, now you have more outlets to do so, and speaking of risk, some of the explanations we were given on this soft markets was that refiners don’t want to buy long haul cargoes because if the strait opens they might find themselves bag-holding some million barrels.. and that was true when physical differentials were +10 and backwardation was at +15.. today is flat, the cost of hedging a cargo is just a couple of bucks, and yet, we don’t see any of that… in fact, we don’t see many incentives to take risk yet given the curve, spreads, tanker rates… for example, if you sent a tanker through the straits back in March, you could make $30M on just one cargo, today you should be happy if you make a couple of millions.. they didn’t do it before when the incentives were there.. Why are they going to do it now? Incentives… lack of incentives today can throw us into trouble ahead.