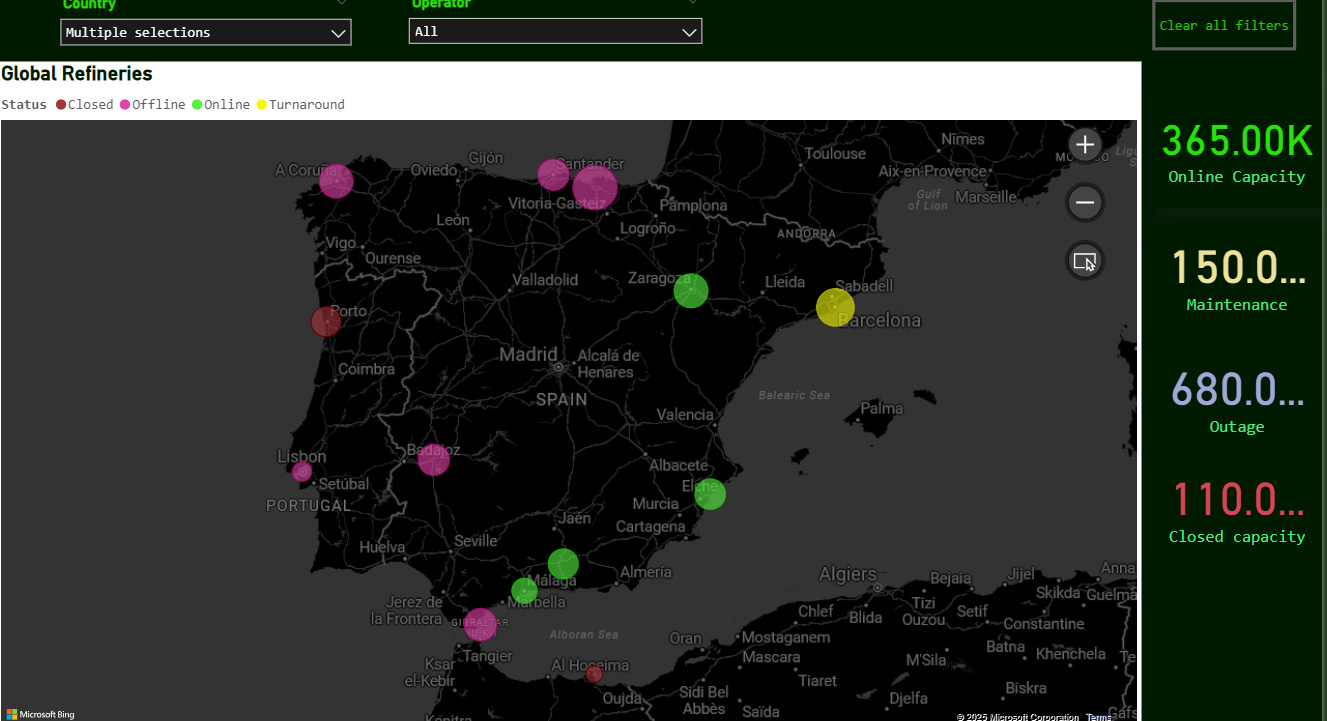

Monday was the day when we all became power grid experts. The Iberian blackout swiftly shut down most of the refining capacity in Spain and Portugal for reasons still unknown, but luckily, the situation resolved itself in 24 hours. To put it into perspective, we lost one aframax worth of cargo, a cargo we might see lingering in the next trading cycle for North Sea, and speaking of lost cargoes, this week marked the end of an era, as Petroineos ceased to process crude in their Grangemouth refinery that mainly run 200kbd crude from the North Sea, which it is connected via the Forties pipeline, add 2 Afras a week to the tally.

https://nextbarrel.com/refineries_global.html

None of this really moved the market, but for physical differentials that were getting soft already since last week, this put the nail in the coffin, and we end the week with negative phys, with Midland trying to price in at the equivalent of Dated-30 cents. Quite a move from last week when we had Trafi buying 10 cargoes in 3 days at Dated +1.85, today Midland is landing at Dated +0.75c CIF Rotterdam.

So, we entered the May 5th OPEC+ meeting looking like this:

· Physical diffs: Gone

· Time Spreads: Gone

· Trade war: De-escalating

· Iran: Depending on the day

· Refining margins: Beautiful crack spreads

On Wednesday, a Reuters headline shocked the markets when “sources familiar with the matter” alerted Saudi Arabia can weather lower prices for longer. Enough said. This was confirmation of the 400kbd output hike, they tried later to patch up the market reaction that lasted one day when they suddenly announced they would meet on a Saturday (today) instead of Monday. Not a good omen either.

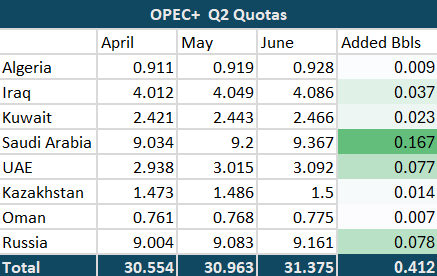

Numbers are out and our suspicions were ascertained, another 411kbd output hike, similar to the last one in May, bringing and accelerated unwind of the 2.2mbpd cut established in 2022.

So, what’s behind this sudden shift in policy from Saudi Arabia?

Market share: One of the alleged motives by market participants is that Saudi wants to reclaim its position as the main supplier of Asian markets in detriment of non-OPEC Atlantic barrels. This theory lacks some ground since Saudi already has an instrument to redirect flows, the mighty OSPs. Lower those enough and Chinese will come back, as they did for May. The other problem with this line of thinking is, how can they compete with Iranian and Russian barrels that sell $10 cheaper? Not even the most prolific producers can compete with that.

Teach the cheaters a lesson: That would be a very expensive lesson to teach, and in any case, are they in a position to teach lessons when they are running a 3% GDP deficit, tapping into debt and cutting spending everywhere. Press like to use Kazakhstan and Iraq as scapegoats, pointing fingers and blaming, but little is mentioned about UAE, which is the main overproducer, and guess what? They can also sustain long periods of low prices.

To me the explanation is far simplier, they need money, and what better time to get it than now, as signalled by the FED, interest rates aren’t coming down so differring oil revenues by one year costs at least 4%. It makes more sense to pump and pass that cost of storaging barrels to the customers, since now the forwar curve incentivices some inventories repletion at lower cost.

We are in the midst of 2025 and we already have seen Q1 Chinese demand numbers, the realization is not only they are not growing at the “reduced pace”, but road fuels demand is 5% below 2024, and that’s Q1, before any of the trade wars collateral damages. Petchem, were Saudis invested a ton of money in Chinese capacity haven’t shown its uggly face yet.

They will sell these barrels as they are wotrh something, if they can bankrupt shale or kill any other start ups that’s and added bonus, is not their primary objective. May export program is capturing the full volumes, suggesting they can ramp up rather quickly.

Next for the OPEC is Trump visit to Saudi Arabia, an arms deal, investment commitments or any other promise can’t make up for the pitfall in lost revenues. All they can do is bite the bullet and try to correct this policy mistake they have been carrying since 2022.

It might look bad for prices, but on the longer run looks better for the market organization. There is no risk of a price war, no one is willing to fight yet another war.