Grill baby grill

Much have been speculated on what a new Trump administration could mean for oil, and now is my turn

Only a few days have passed since we learned the results of the new administration in the great northern country, and speculations about the future of the oil & gas sector didn’t take long to appear. From this account, we also want to speculate about what a Trump administration might mean for oil.

Energy Policy: The sole driver of energy policies will be price—it's that simple. But, for the sake of argument, here’s what I think.

Iran: There are only two ways to stop Iran and eliminate its oil exports. Either close the Strait of Hormuz or completely bomb Kharg Island. Neither option is effective for keeping prices low, and both would alienate the region along with its few remaining allies.

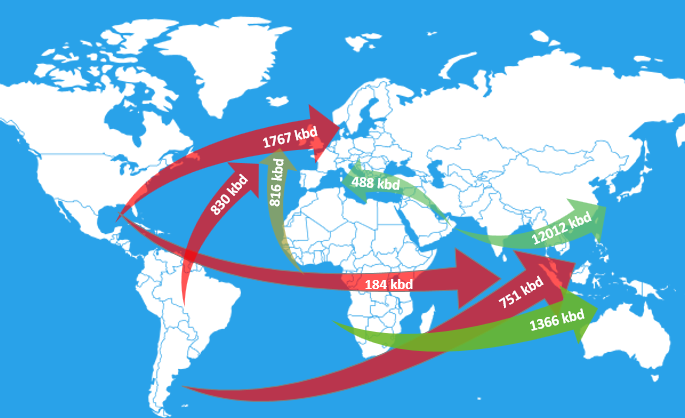

Tightening Sanctions? 99% of Iranian oil goes to China, specifically to Shandong Province, where independent refiners have a well-established transactional network through intermediaries, operating smoothly with yuan-denominated transactions. There's no way to disrupt this via banking sanctions.

Sanctioning the Ghost Fleet? Most of these ships are already sanctioned. Boarding and seizing these ships, as done in the past, would legitimize piracy and green light Houthi in the Red Sea. This has proven ineffective for regional stability, introducing new actors into the conflict (like Greek shipowners, traders, and western shippers).

At most, we might see a reduction in exported volumes—currently around 2 million barrels per day—perhaps halving due to logistical capacity and increased friction with Very Large Crude Carriers (VLCCs) still operating in a gray zone.

Ultimately, the success of sanctions depends on China’s cooperation... tariffs, anyone?

Venezuela: Venezuela appears as the low-hanging fruit for sanctions, given its proximity and relatively low export volumes. It also helps that the largest buyer of Venezuelan crude is, paradoxically, the United States. The issue, however, is the quality of the oil. If there's anything lacking in the Gulf of Mexico, it’s heavy crude, though it could be replaced with help from OPEC.

More sanctions on Venezuela mean more Venezuelan migrants to the United States, so it's a delicate balancing act.

Russia and Relations with Putin: This could have a more immediate effect, although it won't be as simple as a phone call to resolve. Russian oil won’t touch European ports in the immediate future, except for a few niche buyers receiving oil via pipelines. There wouldn’t be a redirection of flows, but pricing dynamics would be impacted. Currently, Russian oil trades at a $12 discount to Brent; it would return to a more normal range of $3 to $4. Will it remain appealing to India and China?

To reach this point, however, Putin wants his $600 billion back, more territory, and concessions from Europe. I doubt Europe would be thrilled with the outcome of a quick resolution to the conflict. And again… tariffs, anyone?

The US-Europe Relationship: Here lies the greatest friction in these new times, potentially accelerating some trends we’ve seen over recent years.

Focus on Shale: There's been attention on shale and how much production could increase in the Permian Basin, stirring concerns of overcapacity and low prices.

This new administration could impact shale by reducing bureaucracy and accelerating federal land and port concessions, fast-tracking delayed projects, scrapping environmental regulations, and freeing up CAPEX for these projects. Investments that were previously unprofitable (like CO₂ storage, hydrogen, etc.) may become even less attractive.

LNG would benefit more than liquids. Several factors restrain oil production growth: high capital costs, pipeline capacity from the Permian (3.5 million barrels per day) to export markets is maxed out, refineries don’t need or can’t process more light oil, and the external market can barely absorb over 4 million barrels per day. There isn’t much room for growth in an environment with average prices at $70; geology and technology have limits. Therefore, I don't see more than 200,000 to 300,000 extra barrels per day of production by 2025.

And that’s assuming global oil demand grows at the projected rate of 1.1 million barrels per day. In a context of increased trade friction, tariffs, and regionalization, demand would likely shrink along with global trade.

When Trump takes office in January, he'll find that today's world is far from the one he left behind when he exited the White House.

Enough talk, let's see why oil prices are plummeting

Keep reading with a 7-day free trial

Subscribe to Oil not dead to keep reading this post and get 7 days of free access to the full post archives.