Jumpstart

With risk premium (almost) gone, now is up to the physical market to set the direction

Right after I published the weekly report highlighting nothing was happening, Israel decided to retaliate against Iran in what the market interpreted as a restrained and well-measured action. As a result, oil prices shattered all previously built-in risk premiums, but has anything changed besides the flat price? -Essentially, yes. Contrary to what we might expect with a 6% drop like the one on Monday, the physical market took a different path and did not fold under the unwinding of positions. A week later all indicators show slight improvements, suggesting that perhaps the worst may already be over.

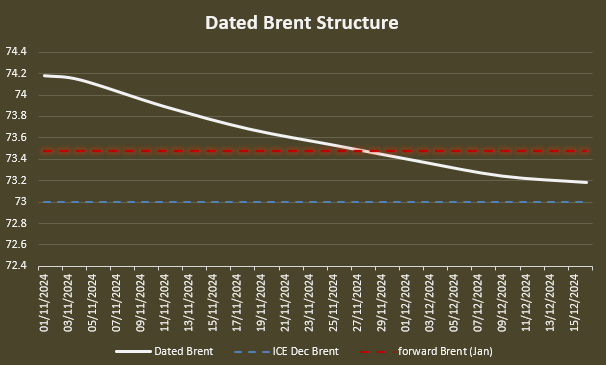

In the North Sea there were some trades indicating a recovery in certain grades, transmitting this relative strength to other benchmarks. Dated Brent, DFLs, Month Spreads, all of them point north. All the differentials halted their decline, and it’s possible that some refineries in the Northern Hemisphere are returning from maintenance faster than the market anticipated. The explanation at hand is refining margins, which weathered the storm remarkably well and even improved slightly since product inflows in October, declined in volume.

Across the Atlantic, the EIA reported weekly figures that were also constructive, especially in products where the draw continues to support firm demand for road fuels. Crude stocks have yet to rise, aided by exports again exceeding 4 million barrels per day.

However, not everything is rosy. In Asia, the weakness is becoming increasingly evident, now including India. With Asian margins at these low levels and flat domestic demand, we are still not seeing East-to-West flows except for some jet fuel shipments to Europe. All this leads me to think we might soon see Middle Eastern crude flowing west of Suez in decent volumes. In recent weeks, we’ve had exceptional pricing opportunities for certain grades in the Mediterranean that could easily have been arbitraged to China, yet, there was no activity or interest; those barrels went west. There is some hope though in Korea + Japan, these two little countries are the best performers in Asia for November, welcome back, we missed you.

There’s something about China that I’m not liking, and it’s not the LNG trucks or EV penetration—those are already well-known factors. However, all our hopes were on the petrochemical sector, which, according to Sinopec and PetroChina reports this week, is not performing in line with expectations for the last quarter of the year.

OPEC is still wavering on whether to return barrels in December or wait another month, wearing down what little credibility it has left, while the world continues pumping barrels.

A bit of good news for OPEC, Brazilian production is tappering off. Another emerging topic is the quality of light crudes, which are becoming increasingly lighter in the Atlantic—something that doesn’t help in winter.

Some additional good news came from macroeconomic data hinting at a rebound in Europe, a solid U.S. market awaiting elections with a volatile dollar and interest rates. However, we’ve learned that all this can change suddenly; we’re still not free of geopolitical risks. Sentiment in the speculative market remains bearish.

At the time of this writing, there has been some headlines by Iran, some peace seeking ones from Israel but not missiles crossed the sky.

If you think there is going to be further flare up, Oil at $73 seems like a good risk/return to the upside since most of the premium has been eroded. If you think things are staying the same, we might still see a flush of remaining bears (albeit a much smaller camp) so I would stay quiet. Fundamentals are not seeing a rush to cover cargoes or refiners’ anxiety, but the sell side is not willing to give away cargos at these prices, which is much more that we could have asked for, since China is not here, and won’t be playing ball for the next few weeks.