Surcharge

Tankers Will Eat the World

A week that could fairly be described as unassuming, with half the industry gathered in London drinking and staring at bar charts, and the other half east of Suez already thinking about next week’s holidays. It was only natural that not much would happen, and indeed, on a net basis, we look pretty much the same as last week.

There are two things worth analyzing that came out of IE Week. The first is the message of enthusiasm and outright bullishness across the sector, completely slashing concerns about an oil glut. Nothing but positive thinking, and everyone happily talking their book, which, unsurprisingly, is long. That is the new market consensus.

Barely had IE Week ended and flat price dropped three dollars… just because.

The other idea that emerged from the event is that the market is somehow disconnected from fundamentals, and this is a view I’m willing to challenge.

What we are seeing in the market is pure fundamentals. It is working exactly as it should, efficiently pricing at all levels, except in one small corner that most S/D models ignore: Freight. That is the only real anomaly in the market, and its effects ripple through the entire supply chain, from dirty to clean… everything is stained by the high cost of moving barrels through time and space.

With high freight, what we really have is a compartmentalized market, where each benchmark only prices barrels that are within reach. For example, the North Sea only has BFOET, with Midland arriving in dribs and drabs, there’s nothing from WAF and very little from the Middle East. Naturally, we’re seeing a stressed light sweets market: we’re operating on baseline flows only. The incremental barrels that normally arrive thanks to open arbitrages are missing, and those are precisely the barrels that set the price. The same applies in Dubai/Sing, the same in the USGC. If the barrel is not here in 20 days, it doesn’t price.

This leaves us scratching our heads, because we have curves in backwardation (a tight market in theory), while at the same time, physical differentials are negative almost everywhere. So… what gives?

Here’s a clue.

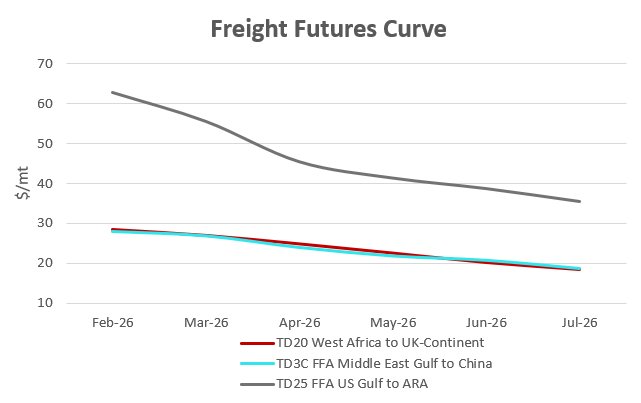

When we look at the Brent curve, what we are really looking at is the freight curve. In other words, today I can’t put a Midland barrel into the Dated window, but I can put it in much cheaper in April. That pressures Brent Froward M2, and that’s why we get a lower price back there.

When freight levels return to more earthly values, then yes, we’ll be able to see some slack capacity again, and we’ll go back to talking about the impeding oil glut. But here’s the catch-22: for tanker prices to actually fall, we need not to have an oil glut. As you can see, it’s a self-reinforcing mechanism, counterintuitive but a good reminder that there is no such thing as linear analysis in these markets… so when are these damn tankers going to come down?

We need to look for an explanation outside of volumes, because volumes are a constant variable this year. So what could derail the freight market?

I have two things in mind. One is still up in the air: the package of measures (number 20) proposed by the EU a few days ago. The other is the India–Russia relationship, and what might happen to that flow if fully replaced. Those are kind of the big themes in tankers today.

A complete ban on maritime services instead of the infamous “Price Cap” would mean that the few cargoes we currently see that are compliant (below the Price cap), and are being served by the mainstream fleet, would disappear, leaving Russia dependent solely on its shadow fleet.

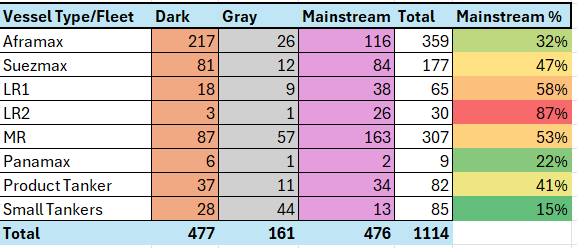

I’ve been looking at the 2025 numbers to get a sense of what we’re talking about.

The first thing that stands out is how the entire clean trade was left in the hands of the mainstream fleet. I can think of two reasons. First, almost all gasoil and naphtha trade sits below the price cap. Also, a logical explanation is that when gasoil exports collapsed due to attacks while crude exports exploded, Russia decided to move all LR2s into the dirty trade, effectively turning them into Aframaxes. By the time they came back toward the end of last year, it was already too late to make the switch, and we ended up with this fleet composition. On average, we’re talking about 30–35%, which is still a high watermark.

My point is, that around 200 ships (Aframax and Suezmax) and another 200 clean vessels would return to tier 1 routes. That should be enough to pressure Afras and Suez’s, and eventually VLCCs. That’s the theory. But I have an issue with it: “Ice Class” vessels. These ships are mandatory in the Arctic Circle during winter—right now—and 30% of ice-class Suez/Afras are sanctioned (most of them belong to Sovcomflot). That’s not so much a problem for Russia, but it is for the North Sea and Vancouver, or some deliveries into Korea/Japan… guess why an Afras has been around $70k for the last two months? Exactly.