The tail wagging the dog - Week 1

A slow week on the physical, but an interesting one in paper markets

As we deal with the hangover from celebrations in the last two weeks, with Europe and much of the US still not reporting to their desks (deal flows have been dead) you would be right to think that not much could happen in the oil market, and you would be wrong.

In trying to disect the recent breakout of the range (finally!) we need to look back a couple of weeks when the Dubai marker was overrun by the issuance of fresh Chinese import quotas for “teapots”, and State-run Sinochem received an oil import quota of 17.12 million metric tons for 2025, which will be for the group's eastern China refineries and of course Total Energies buying and pushing the benchmark hitting bids left and right, by now is no secret that Total was buying on behalf of the Chinese that don’t want to be seen in the open market.

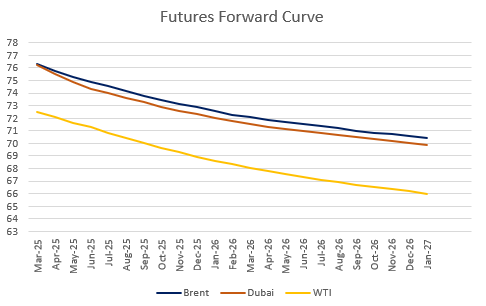

That Dubai action was enough to set a floor on differentials across the board and set the stage for a nice build up, but is that enough to move things a step higher?

I would love to say that oil demand is exploding, Chinese helicopter money, oil production is collapsing and inventories are near tank bottoms..(well, that last part is true) but is not the case. I’m getting some winter 2023 vibes when oil was riding on the back of Natural Gas hysteria.

An Artic storm, gas transit through Ukraine halted after 50 years and a war that intensifies, talks about bombing Iran and the Trump wild card makes a perfect cocktail to derive prices on pure speculation.

It is still too early to tell but for all the talks about a Q1 with 1 Million barrels of surplus seems distant in the current environment, specially when we see crude inventories still dropping and refineries running hard for this time of the year. Product stocks are indeed building and that would be something the market will have to deal with sooner than later, but for now, refining margins are acceptable, market structure doesn’t incentivize to build stocks, though some cases like gasoline are the only way out, but market is choosing to ignore that and instead focus on gasoil/heating oil instead.

Fundamentally, in terms of flows, regional pricing, differentials not much changed from last two weeks, is kind of worrying that with freight rates exceptionally low most arbs remain closed, limiting trade opportunities. That could also explain why many are choosing to play flat price instead of spreads.

On the physical side, things are really quiet, proof of that is the absence of major players in the North Sea window. The loading programme for Feb BFOET looks smaller in 200kbd, due to a pipeline maintenance and a cargo that has been frontloaded to January.