Brent Complex Complexity

From zero to hero in 5 minutes

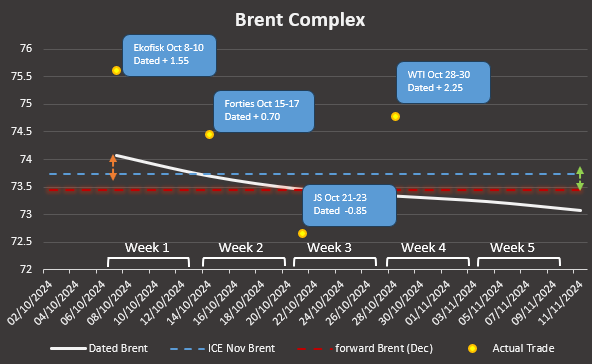

People much smarter than me attempted to explain this and perished trying but I’m willing to give it a shot, plotted in a chart like the one below will make it easier to understand better what we mean when we say “Dated +2”, “DFL this or that”, “the chains…” and so on.

I admit I’m guilty of throwing this lingo around expecting everyone to pick up the concept behind the numbers and since most of this data is not freely available no one really cared to explain it to the broader audience. In a way to redeem myself and knowing that there is an audience of “non-oil” professionals looking to get an understanding of the physical markets (and rightly so), I decided to make a brief explanation on this monster called Brent Complex. If you want to know where the price you see on a screen comes from, keep reading.

Let’s take a look at each of the components, and by components I mean this array of obscure derivatives.

Forward Brent

That is the red dotted line, and arguably the most important derivative of them all.

Forward Brent is a swap (similar to a future) but it trades OTC (over the counter). This is the real deal because these are actual barrels changing hands from producers, to traders, end users, etc.. when you enter into a transaction like this you get a fixed price, let’s say you are a producer in the North Sea and you know you will have an available a cargo in December and want to fix the price today and forget about it, so you pick up your phone and call a swaps dealer or login into ICEchat and set the price for delivery oil into the future, in this case I used December because the industry looks at M2 for timing of delivery. Anyway, this is what ideally the ICE Brent December Future would converge to at expiration. ICE is based on this swap, and the price of this swap is set daily by Platts or Argus.

ICE Futures

Now we get to the future you know, the differences are the timing of expiration, and that ICE is financially settled and cleared on an exchange. Is a different tool for different market participants, in fact, American oil Majors and some NOC prefer to trade futures than swaps (because accounting and taxation purposes)

There is a link between these two instruments and it is another swap, the green arrows, called EFP (Exchange of Future for Physical) that lets you jump from one instrument to another, if they have the same maturity, Nov to Nov, Dec to Dec, etc… In this case I’m showing Nov ICE Brent for illustration purposes.

Imagine you are a Chinese refiner, and decide to go long ICE November futures to hedge your crude intake, you are long Brent on paper but you don’t have a cargo yet, then you decide you will take a physical cargo so what you can do is to buy an EFP and automatically you are out of your paper position and long physical, you will get a cargo delivered at a terminal to pick up, at some point, the seller of the original swap will call you and give you a date to pick up a cargo on an Aframax, you have been dated, and there is where Dated Brent is born.

Dated Brent

Platts and Argus assess the price of physical cargoes of the Brent basket, crude grades that are scheduled to be delivered within a certain time frame, usually between 10 to 30 days ahead of delivery. The assessment captures the price of cargoes that have been fixed, traded, or offered for delivery during this window. Reporting agencies use real-time market information from the physical trading of BFOET (Brent, Forties, Oseberg, Ekofisk, Troll, and now WTI) crude oil. They track bids, offers, and trades submitted by market participants during the assessment window (4:00 PM to 4:30 PM London time). The methodology relies on actual market data rather than speculative pricing, and that is why is so relevant not only for the North Sea but for other regions pricing against Brent.

That is the white line here, and yes, you can build an intramonth forward curve for Dated Brent, to do that we use another swap, the almighty CFDs, short for “Contract for Differences”, bear with me because here is where things start to get muddy… CFDs are swaps (a fixed price bet) on a weekly basis, you have a strip of CFDs that commences to trade 10 days from today, so Week 1 starts at today (Oct 2) + 10 days, Oct 12, and for 6 weeks more so, to mid-November or so..

These CFDs are the link between the red dotted line and the White one, so to build a Dated Brent forward curve you have the December Forward +/- the price of each week, today we have 73.45 + week 1 at +0.62, then 73.45 + week 2 at +0.45 and so on until you get week 6, in doing so, you can have a view of how barrels are clearing throughout the inmediate term, you know, is it in contango? is it in backwardation?

And then… we have yet another Swap, the orange arrow, and that links Dated brent with the ICE Futures contract, and that is the motherfucking DFL, dated to frontline. That is why I used Nov ICE, November contract is M1, frontline month. With this instrument you can managed your exposure to both financial and physical markets.

Physical Deals

This is the Juicy part, every day Platts and Argus report deals from market participants that already have a position in Dated or Forward Brent (they might as well have an ICE future and convert it to physical using the EFP) and they are shuffling these cargoes among themselves at a premium/discount. At some point they were given a date for the cargo and they trying to sell it on the open market. You have different grades that have different properties and they have to be adjusted by quality, but let’s just assume they are all the same. What is interesting here, is how far these cargoes are trading against Dated, the distance between the yellow dot and the white line, and across the timeline. What is different in this case, is that premium/discount is the actual risk a trader takes, there is no simple way to hedge that differential within the Brent complex. Think that if everyone traded at Dated, there won’t be any profit to be made.

Conclusion

“-Mr Bandit, I trade futures on Ameritrade, what should I care about this?”

You shouldn’t know this in depth, that is true, but understanding these data points can help you gauge market health, are we in a strong market? a weaker one?

Blue line above red line? - That is good

White line above red line? - That is good

The front part of the white line below the back end? - That is bad

Yellow points closer to the white line? - be careful

White line below the blue line? - get out

Yellow dots below the white line? - Sell everything!

There are much more nuances to this, but this simple explanation will help you to follow through the usual Friday’s recap and get into fights on Oil Twitter, which are getting increasingly savvy about the once obscure physical market. Feel free to comment and chime in.

Is CFD always 10 days from today? Platts seems to have the CFD week defined as fixed Thursday to Wednesday.

bit confused. you are talking nov brent when we are on Oct 6. Rightnow the m1 brent is Dec and month 2 is January.